Summary

- FTI Consulting, Inc. has shown gradual yet considerable and stable growth with ample cash inflows over the past decade.

- Despite being in operations for many years, it has not distributed dividend payments yet.

- The price moves in an upward pattern for the last three to four months, but the bearish remains apparent with potential overvaluation and moderate volatility.

- The company thwarted the adverse effects of the pandemic as its performance and financials remained stable.

Growth and stability FTI Consulting, Inc. (NYSE: FCN) remained manageable which continued even in the time of the pandemic. Revenues and income have been stable while liquidity and cash inflows remained adequate for its operations, financial obligations, and continuous expansion amidst the challenging and disruptive environment. Despite this dividend payments have not been paid yet while the stock price does not seem to agree yet with the considerable performance of the company as the bearish trend persists.

Company Financials

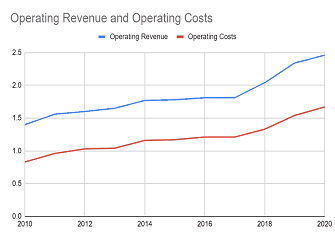

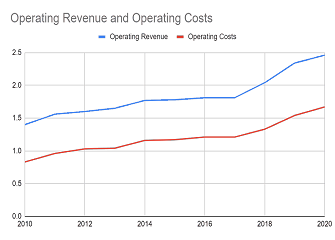

Operating Revenue and Operating Costs

FTI Consulting, Inc. has been operating in a wide range of consulting and management services from financial, legal, and economic to public relations, technology, and risk management. Since the mid-2000s, one can notice that the company has been capitalizing on growth through its continuous yet prudent acquisitions and increased operations and offerings. Despite being involved in the bankruptcies of two large firms, the company maintained a stable performance over the years as its services continued to expand.

The operating revenue of the company has increased gradually yet continuously over the years. In 2010, when it acquired FS Asia Advisory Limited Asia in Hong Kong, its activities in the region expanded. Also, we can observe that revenues have almost tripled in five years from about $500 million to $1.4 billion. Since then, growth has become slower but remained consistent and reasonable. In 2014, its revenues were already $1.77 billion which was also driven by acquiring TLG Partners which produced thought leader indexes. In 2018, it expanded further which drove its substantial increase already as it climbed up to $2.04 billion before further increasing by another $300 million, or 14% to $2.34 billion in 2019. Likewise, there was an uptrend in the operating costs, but the gap from the operating revenue remained wide as the movement has been more gradual at $500-$600 million in 2010-2017. In 2018 and 2019 growth became more apparent which showed that increased demand for its services and continuous expansion offset the associated costs with these as gross profit jumped to $700 million and $800 million, respectively. Nevertheless, the decreasing gross profit margin suggests that the company must still work hard to improve efficiency with its continuous increase in operating capacity to speed up growth.

In 2020, things remained stable for the company despite the unfavorable impact of a more challenging environment as the pandemic continued to disrupt the market. As problems in operations and financials arose, demand for the company's strategic management and services, particularly in the financial and economic segment rose substantially. With that, revenue in all quarters increased and accumulated to $2.46 billion which gave a $100-million, or 5% increase. But things did not get entirely better as direct costs increased by 7% and offset revenue growth and slowed down viability. Despite this, the core operations remained manageable with a gross profit of $790 million. Hence, it shows that amidst the unstable market and economic condition, the company was able to stabilize and synergize the operations and thwart or at least reduce the unfavorable effects of the pandemic.