Summary

- McCormick is a high-growth dividend stock in a defensive sector.

- Investors benefit from strong (and rising) free cash flow, a healthy balance sheet, and a good mix between organic and acquired growth.

- Unfortunately, the stock is everything but cheap as the stock price growth has priced in 'a lot'.

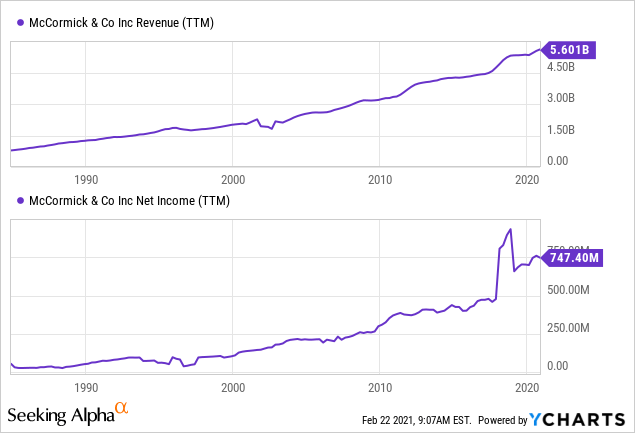

Data by YCharts

It's time to discuss a very interesting dividend stock. The Maryland-based manufacturer of consumer and commercial flavor products is a true dividend growth stock. The company has a relatively low yield but a high dividend growth rate. This growth rate is fully supported by a steady increase in free cash flow through both organic and acquired growth. Unfortunately, the stock is far from cheap and rising inflation is pressuring defensive 'yield plays' like government bonds and consumer staples. As a result, I believe that McCormick & Company (MKC) is slowly turning into an interesting long-term play and should be on every dividend growth investor's shopping list.

Source: McCormick & Company

A Brief Overview Of McCormick

While I am writing this, McCormick has a $23 billion market cap, which makes it the fourth largest stock-listed company in the packaged foods industry. The company is what I consider to be extremely boring - which is a good thing. I own a lot of stocks that I consider to be boring (see my Seeking Alpha bio). These are stocks that more or less see business as usual during a recession. Sure, sales might be impacted, but overall the only headwind an investor might encounter is temporary and unrealized capital losses.

McCormick is one of the world's leading producers and distributors of spices, seasoning mixes, condiments, and other flavorful products to consumers, food manufacturers, and foodservice customers. These segments are listed below. I also added the 2020 sales breakdown.

- Consumer (64.2%)

- Flavor Solutions (35.8%)

In its Customer segment, the company calls Walmart (WMT) its largest customer, which accounted for 12% of 2020 sales. In its Flavor Solutions segment, the dominant customer is PepsiCo (PEP) with 11% of total 2020 sales.

When combining all segments, the company generates 64.2% of its sales in the United States. EMEA countries account for 18.7% of total sales, followed by APAC countries (10.3%).