Summary

- Lockheed Martin is trading off of its highs but has rebounded from recent lows.

- The company pays an attractive and growing dividend and continues to be a beneficiary of increased defense spending.

- For investors with a long term horizon, Lockheed Martin may be worth adding to the portfolio.

Lockheed Martin (LMT) has been a beneficiary of the growing defense budgets of countries around the world. Being a premier manufacturer of planes, helicopters, missiles, and more, the company continues to see revenue rise in almost any economic environment. Due to defense being necessary and technology always evolving, the company has a stream of revenue that is as close to guaranteed as you can get. With shares trading off their highs, they have popped on to my radar. I have long waited to initiate a position in the company and would wait until the recent run up has a pullback again to begin. However, the shares are beginning to look enticing with a 3%+ yield.

Performance

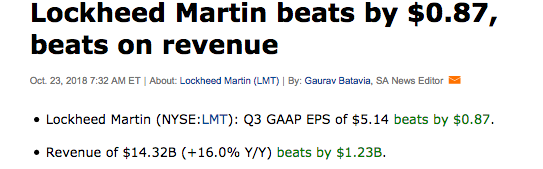

In the third quarter earnings report, Lockheed reported earnings that beat on both the top and bottom lines.

Source: Seeking Alpha

The company saw revenue grow 16% and earnings grow 54.8%. This was due in part to tax reform along with the help from the top line growth. The company also raised its forecast for earnings per share of approximately $17.50 (from $16.75–$17.05), on net sales of about $53B up from $51.6B.-$53.1B. Cash from operations in the third quarter of 2018 was $361 million after pension contributions of $1.5 billion, compared to cash from operations of $1.8 billion in the third quarter of 2017, with no pension contributions. Seeing the pension being funded is always a positive as it prevents a future overhang of liability from becoming a problem.