Summary

- Kraft Heinz can't afford its dividend if it wants to pay down debt. I have written several articles here showing this. The Q3 numbers confirmed this.

- However, both the CFO and new CEO implied that there would be capital structure changes. This will obviously involve large asset sales to pay down debt.

- But theoretically, it could also involve a "carve-out" capital raise of a large portion of the company. This could mean listing Kraft as a separate stock, raising equity as well.

- Of course, theoretically, the company could be taken private again, but I somewhat doubt it. If a carve-out is done, Kraft Heinz could split its dividend between the companies.

- That might be the only way the dividend wouldn't be cut. It could also allow one or both of the companies to both reduce debt and keep the dividend stable.

- This idea was discussed in more depth with members of my private investing community, Total Yield Value Guide. Get started today »

My Thoughts Since the Q3 Financial and Conference Call

I've thought a good deal about both the recent financial performance of The Kraft-Heinz Company (KHC) as well as the conference call with analysts. I have written articles here before that Kraft Heinz can't afford its $1.60 per share dividend. I've refined my thoughts a bit.

After looking at the Q3 financials, I believe that KHC can afford its dividend, barely. But this is only if KHC does not want to seriously reduce its large amount of debt.

Debt and Dividends

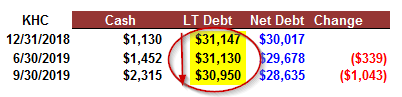

For example, so far this year, despite paying the dividend and interest associated with the debt, it has fallen by only 0.63%, or by $197 million from $31.147 billion. On a net debt basis, it fell a little more. You can see this in the following table:

Source: Hake

On a net basis, the debt fell by $1 billion, or just 3.5%. But dividends paid so far this year have been $1.464 billion.

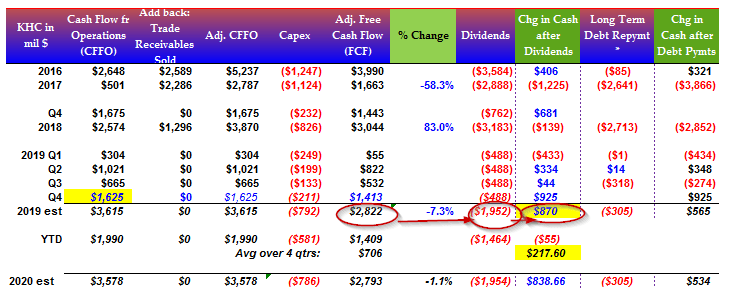

Moreover, the company can not afford more than about $870 million a year, or $218 million per quarter of debt reduction. At that pace, it would take over 30 years to pay down its large debt pile.

You can see this in my table below, including my projections for Q4 2019:

Source: Hake estimates

I forecast that free cash flow in Q4 2019 will be similar to Q4 2018, at 24.3% of sales. I estimate that Q4 sales will be $6.693 billion. After deducting capex, at 3.2% of sales, I project that Q4 free cash flow will be $1.413 billion.

This allows KHC to essentially earn about $2.8 billion in FCF during the year 2019. The dividend costs $1.952 billion at the $1.60 rate. The excess is $870 million, or $218 million per quarter with which KHC can pay down debt.

So management is facing a choice. Do something about the debt through asset sales, like it did this past quarter: