Summary

- I revised my model for AT&T using some assumptions based on the Elliott Management Corp. plan for the next two years.

- The plan envisions asset sales, buybacks, and debt reduction by AT&T, along with a more focused management to increase EBITDA and FCF.

- My model shows AT&T, with certain assumptions, would be worth $59.41 per share, or 62% above the present price.

- Subscribers to my Total Yield Value Guide get the spreadsheet model.

- This idea was discussed in more depth with members of my private investing community, Total Yield Value Guide. Get started today »

The Elliott Management Plan Suggests AT&T Should Change its Focus

I studied the Elliott Management "Activating" Plan for AT&T (T) published on September 9, 2019, and revised my model for the company for the next two years. This is a revision based on the model I developed from my previous article on AT&T on July 17, "AT&T is Worth Over 50% More Than Its Present Price."

I made certain assumptions which were based on the Elliott Plan and compared the company to its peers with certain revisions. My model estimates the company would be worth $59.41 if AT&T undertakes most of the suggestions. Interestingly, Elliott suggests the company would be worth between $55 and $60 per share by 2023 if their steps are activated. Note: subscribers to my Total Yield Value Guide have access to the detailed spreadsheet.

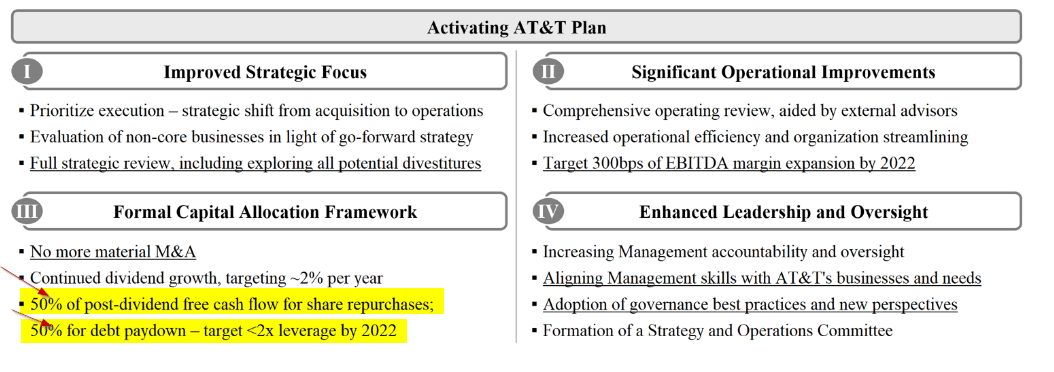

The core focus of the Elliott Plan is to increase EBITDA by more focusing the company on its core assets and to begin asset sales to fund both debt repayments and significant buybacks. Here is a table they presented:

Source: Sept. 9 letter from Elliott Management Corp to AT&T

Interestingly, AT&T's investor relations website now highlights on its front page a statement from the CFO that T expects to begin buybacks this year along with $6-8 billion in asset sales: