Summary

- Having raised its dividend for the past 23 years, Church & Dwight is a Dividend Contender.

- Despite its risks, Church & Dwight is well-positioned to deliver strong growth going forward because of its tremendous brands and experienced management team.

- Unfortunately, I estimate that Church & Dwight is trading at a 19% premium to fair value.

- Between the 1.1% dividend yield, 8-9% earnings growth, and 1.7% annual multiple contraction, Church & Dwight is likely to deliver 7.4-8.4% annual total returns over the long-term.

- Church & Dwight would deliver a 1.4% yield, 8-9% earnings growth, and a static valuation multiple, for annual total returns of 9.4-10.4% over the next decade at my fair value.

As a dividend growth investor, I'm always looking for companies with strong brands that have a history of rewarding shareholders with dividend increases and increased earnings on a fairly consistent basis.

One such company that comes to mind is Church & Dwight (CHD).

I'll be discussing the dividend safety and growth profile of Church & Dwight, the company's fundamentals and key risks, in addition to the sole reason I rate the company's shares a hold rather than a buy, which is due to overvaluation.

I'll then conclude the article by offering my predictions on annual total returns over the next decade at both the current price and at my estimated fair value.

A Safe Dividend With Potential For Long-Term High Single Digit Growth

In order to determine the safety of Church & Dwight's dividend, we'll start by examining both the EPS and FCF payout ratios of the company.

In its previous fiscal year, Church & Dwight generated EPS of $2.27 against dividends per share of $0.87 paid during that same time, for an EPS payout ratio of 38.3%.

Looking at the company's current fiscal year, Church & Dwight is guiding for EPS of $2.47 against dividends per share of $0.91, for an EPS payout ratio of 36.8%.

Moving to FCF, Church & Dwight generated operating cash flow of $763.6 million against $60.4 million in capex (according to page 50 of Church & Dwight's most recent 10-K), for total FCF of $703.2 million in FY 2018. Against the $213.3 million in dividends paid during that same time, this equates to an FCF payout ratio of 30.3%.

Given that Church & Dwight is in the midst of another year of strong financial results and that the last dividend raise of 4.6% was conservative, the company's FCF payout ratio is set to decrease a bit from FY 2018 to FY 2019.

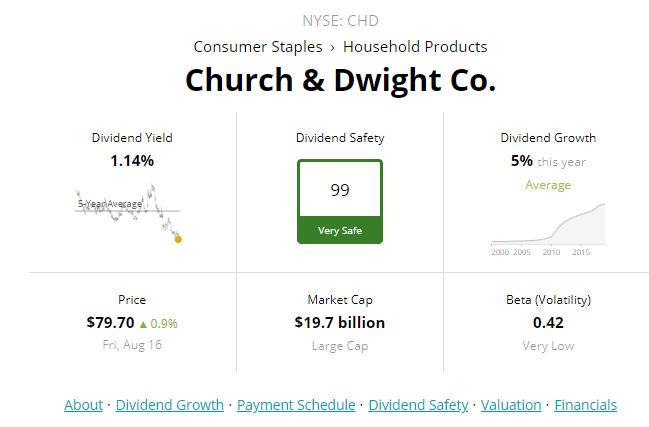

Overall, Church & Dwight's dividend is clearly very safe as evidenced by the above payout ratios, which are very conservative for a consumer staples company.

Image Source: Simply Safe Dividends

Image Source: Simply Safe Dividends

As we discussed above, Church & Dwight's dividend is very safe and due to the company's very conservative payout ratios, Simply Safe Dividends agrees with that assessment.

The next logical step for us is to determine Church & Dwight's likely dividend growth going forward.