Summary

- Having raised its dividend for each of the last 9 years, Hershey is a soon to be Dividend Contender with a long history of rewarding its shareholders.

- Despite the risks associated with Hershey, I believe the company's iconic brand, management team, and decent balance sheet will deliver great results for shareholders in the years ahead.

- Unfortunately, Hershey is trading at a 14% premium to fair value.

- Between the 2.1% yield, 7-8% earnings growth, and 1.5% annual valuation multiple contraction, Hershey is likely to deliver 7.6-8.6% annual total returns over the next decade.

- While this isn't a terrible return by any means, I generally require 10%+ returns as a margin of safety. I would target a 2.4%+ yield before adding to Hershey.

With the Dow Jones Industrial Average, S&P 500, and Nasdaq all soaring to record highs, the difficulty in finding companies trading at reasonable valuations continues to grow, as does the ease of finding companies that are trading at stretched valuations.

One such company which comes to mind that fits the latter description is Hershey (HSY).

While I'll be discussing Hershey's dividend growth and safety profile, and its fundamentals and risks, the key takeaway is that Hershey is moderately overvalued at its current price. I'll conclude the article by offering my total return estimates over the next decade and my desired yield before I would consider adding to my position.

A Safe And Well Covered Dividend With High Single Digit Growth Potential

Prior to making an investment decision, I like to analyze both a company's dividend safety and growth profile.

I'll begin by assessing the safety of Hershey's dividend from an EPS payout ratio and FCF payout ratio standpoint.

Last fiscal year, Hershey generated diluted EPS of $5.36 against dividends per share of $2.756 paid out during that time, for an EPS payout ratio of 51.4%

Moving to the current fiscal year, Hershey expects diluted EPS of $5.50-5.66. Assuming a midpoint diluted EPS figure of $5.58 and dividends per share of $2.989 in 2019 (this factors in a 7% dividend increase later this month), Hershey's payout ratio would be 53.6%.

As per pages 56 of Hershey's most recent 10-K, the company generated ~$1.600 billion of operating cash flow against $328.6 million in capital expenditures, for total FCF of $1.271 billion. Against the $562.5 million in dividends paid during this time (per page 37 of the company's most recent 10-K), this equates to an FCF payout ratio of 44.3%.

There will be a slight expansion in the company's FCF payout ratio from 44.3% to 45-46%, which is what I consider a flawless payout ratio. Hershey retains plenty of capital to fund its growth projects, which ultimately allows future dividend growth.

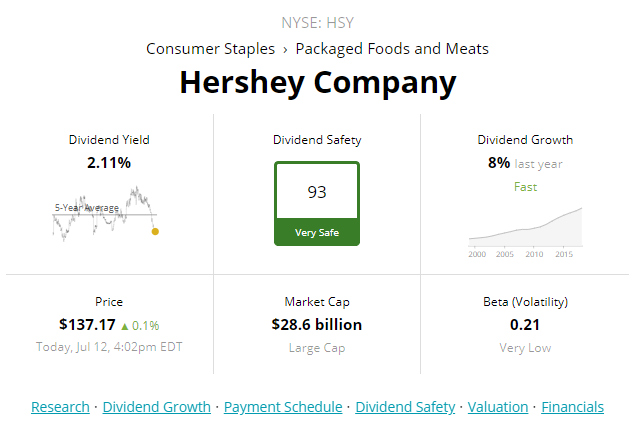

Image Source: Simply Safe Dividends

Image Source: Simply Safe Dividends

Given Hershey's reasonable payout ratio, decent balance sheet, and earnings quality, Simply Safe Dividends and I agree that Hershey's dividend is very safe for the foreseeable future.

While dividend safety is one consideration for a dividend growth investor, the equally important consideration is what kind of dividend growth a company can deliver in the future, which leads me into my next point.