- "No vacancy" becomes "no occupancy." Hotel REITs - along with the global leisure and tourism industry - have been decimated by the coronavirus pandemic, plunging more than 50% this year.

- Following a record year for the industry in 2019, hotels REITs reported occupancy rates below 20% in Q2. Occupancy has recovered to roughly 45% by late summer, but winter is coming.

- Every hotel REIT has slashed its dividend in an effort to stay afloat, as 40-50% occupancy is needed to "keep the lights on." Suburban-focused and leisure-oriented properties have outperformed urban hotels.

- Perhaps a more "pure play" on the success of a vaccine than even the pharmaceuticals themselves, a significant "second-wave" of the pandemic would be likely catastrophic for equity holders.

- While leisure demand should bounce back relatively quickly when the pandemic subsides, business and group demand may take up to a half-decade or longer to fully recover.

- This idea was discussed in more depth with members of my private investing community, iREIT on Alpha. Get started today »

REIT Rankings: Hotels

(Hoya Capital Real Estate, Co-Produced with Brad Thomas)

Hotel REIT Sector Overview

Hotel REITs - along with the global leisure and tourism industry - have been decimated by the coronavirus pandemic, plunging more than 50% this year as "no vacancy" has quickly become "no occupancy." Following a record year of occupancy and revenues in 2019, the hotel REITs recorded a mind-blowing 90% plunge in RevPar ("Revenue Per Available Room") by mid-2020, forcing every hotel REIT to slash its dividend this year as the sector faces an ongoing existential crisis. Within the Hoya Capital Hotel REIT Index, we track the 18 largest hotel REITs, which account for roughly $25 billion in market value.

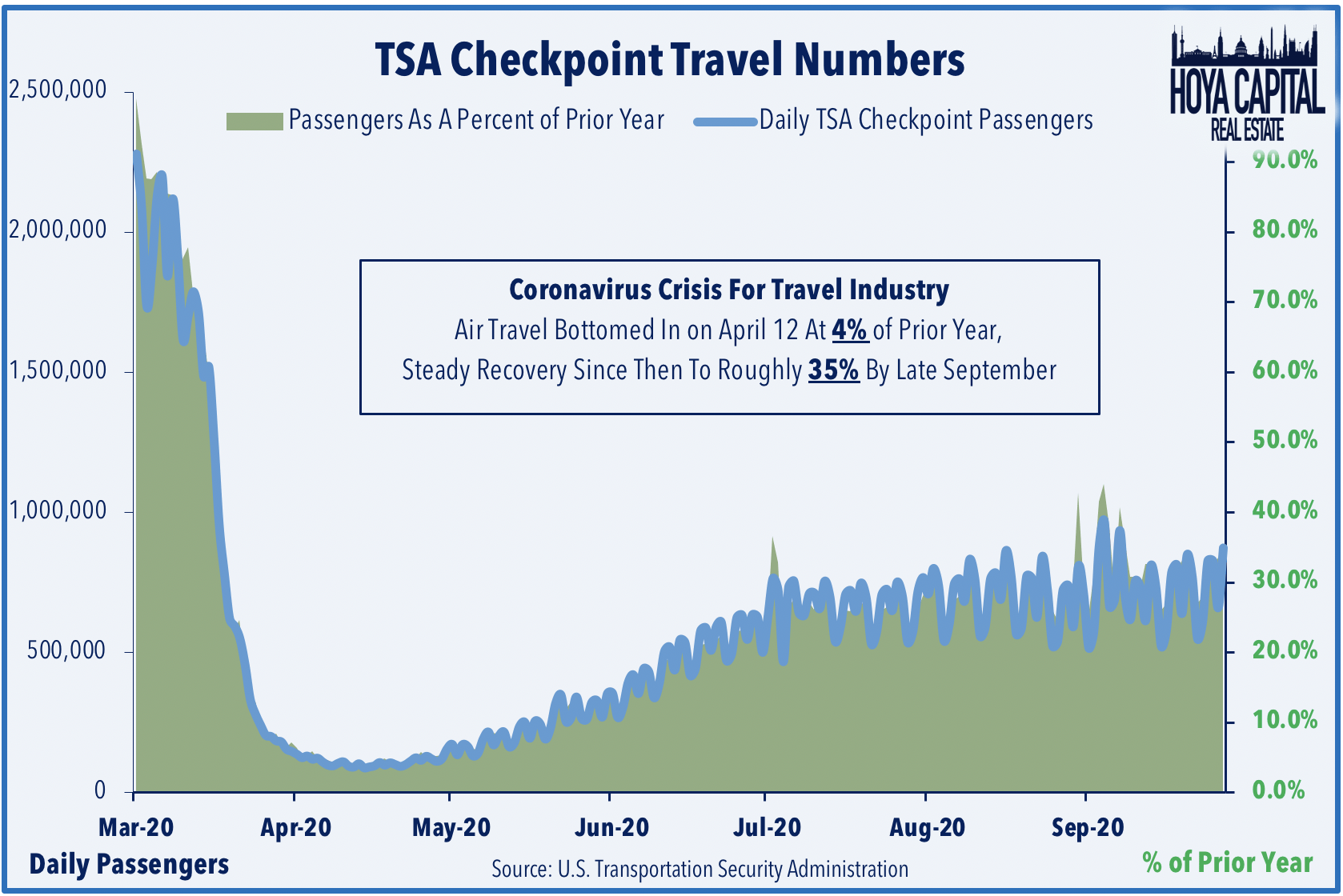

Hotel REITs ultimately remain at the mercy of the coronavirus pandemic, which forced roughly half of hotels in the U.S. to temporarily close during the peak of the lockdown in April, though the majority of hotel properties have since opened - generally with reduced capacity. Hotel ownership is a tough, capital-intensive business even in the best of times, and hotel REITs tend to be "overweight" in the most affected segment of the lodging industry: corporate travel, group bookings, and international tourism. Demand from these segments is closely correlated with domestic air travel, which has exhibited a slow recovery from its lows in April according to TSA Checkpoint data. Airline travel bottomed in early April at just 4% of its prior-year levels but has rebounded to roughly 35% of "normal" by late September.

While leisure demand should bounce back relatively quickly when the pandemic subsides, business and group demand may take up to a half-decade or longer to fully recover. In terms of occupancy, suburban-focused and leisure-oriented properties have outperformed urban hotels that cater more towards the more affected business-oriented segments, resulting in significant underperformance by hotel REITs relative to the national averages. According to data from STR, hotel occupancy bottomed out at just 24.5% in April but has recovered to 48.6% in the week ending September 19th and has held onto recent gains despite the seasonal headwinds. Room rates, however, remain lower by 29% from last year, amounting to a total revenue per available room (RevPAR) decline of a whopping 51.6%.