Summary

- From bad to worse. Entering 2020 on already unstable footing following a tsunami of store closings over the past half-decade, mall REITs have been punished by the ongoing coronavirus pandemic.

- Mall REITs have plunged nearly 50% so far in 2020. Absent a miracle, mall REITs are likely to underperform the REIT average for the fifth straight year in 2020.

- Rent collection averaged less than 50% in the second quarter. Same-store NOI dipped roughly 30% in Q2, while FFO per share has plunged a mind-numbing 45% through the first half of 2020.

- Shop till you drop? Simon Property is on a shopping spree, as the mall REIT continues to make investments into distressed retail brands that will keep many storefronts open, at least for now.

- The forthcoming post-pandemic "suburban revival" offers a glimmer of hope for deep value speculative investors, as does Amazon's rumored interest in converting vacated department store space into distribution centers.

- This idea was discussed in more depth with members of my private investing community, iREIT on Alpha. Get started today »

REIT Rankings: Mall REITs

(Hoya Capital Real Estate, Co-Produced with Brad Thomas)

Mall REIT Sector Overview

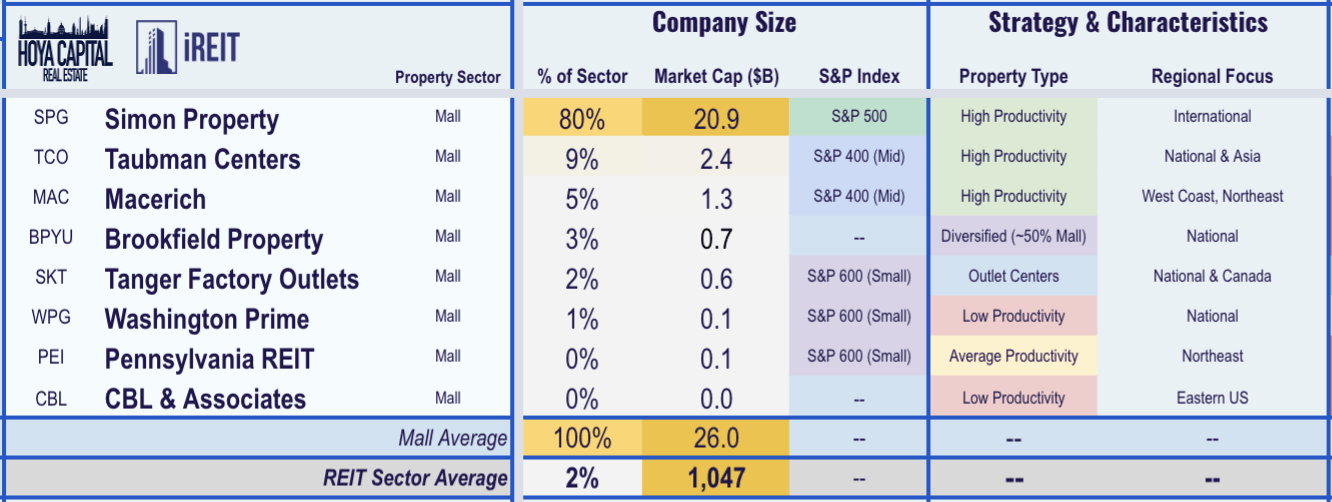

Apocalypse Now? Entering 2020 on already unstable footing following a tsunami of store closings over the past half-decade, mall REITs have been punished by the ongoing coronavirus pandemic, plunging nearly 50% in 2020. Within the Hoya Capital Mall REIT Index, we track the seven mall REITs, which account for roughly $25 billion in market value: Simon Property Group (SPG), Taubman Centers (TCO.PK), Macerich Co. (MAC), Tanger Factory Outlet Centers (SKT), Washington Prime Group (WPG), Pennsylvania Real Estate Investment Trust (PEI), and CBL & Associates Properties (CBL), as well as one diversified REIT, Brookfield Property REIT (BPYU), which owns a portfolio comprised of roughly 50% mall properties.

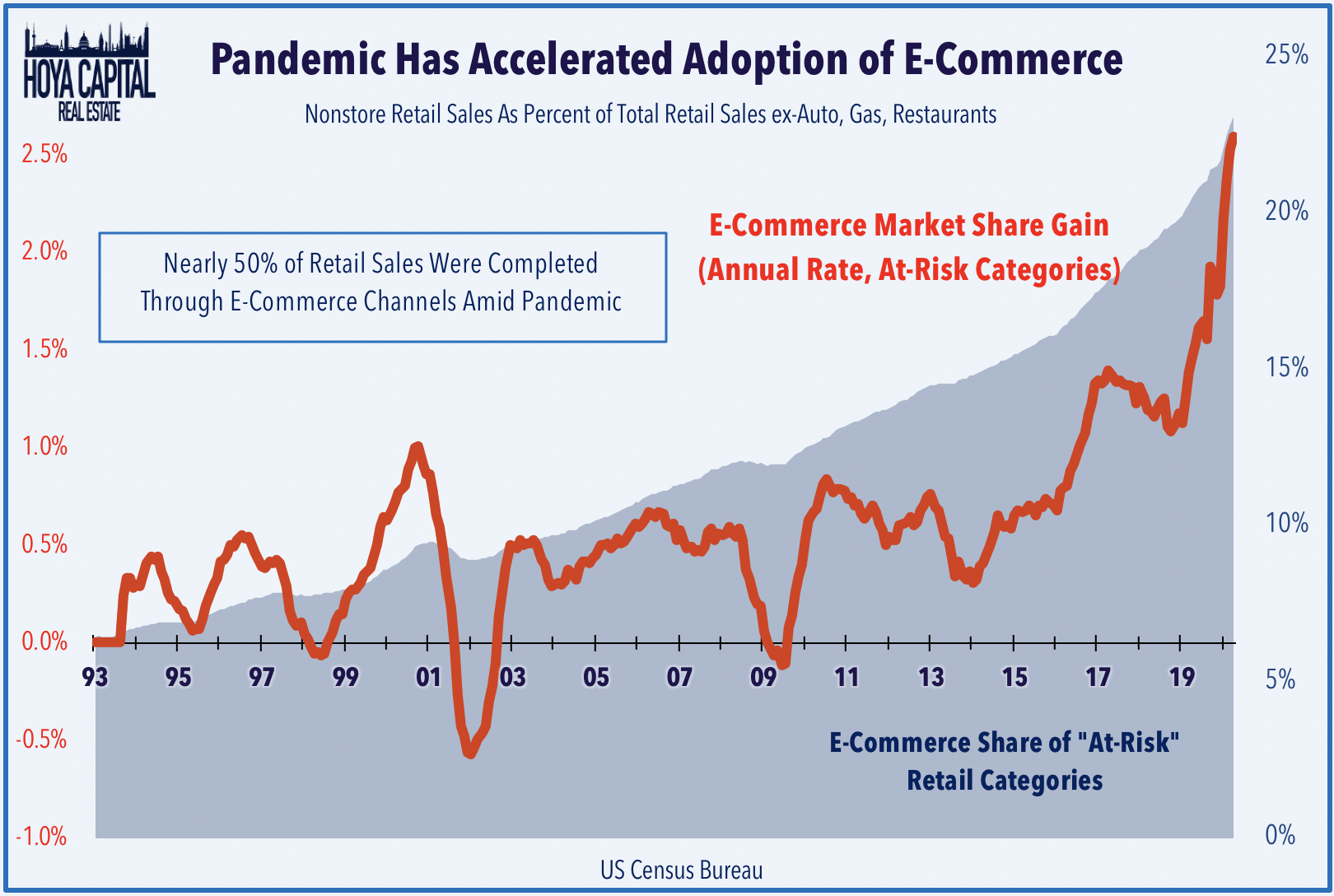

Absent a miracle, mall REITs are likely to underperform the REIT average for the fifth straight year in 2020. As we'll expand on throughout this report, we remain bearish on the mall REIT sector, as the coronavirus pandemic further amplified the significant secular headwinds facing the enclosed mall format and accelerated store closing decisions. The pace of store closings is expected to increase substantially in 2020 during and after the coronavirus fallout, adding to what was already a record year of store closings in 2019. Following a similar pattern as 2019, the market share loss and pace of store closings will likely hit the traditionally mall-based retail categories especially hard in 2020, the majority of which fall into the dreaded "non-essential" category and those that have struggled to adapt to the increasingly digital retail landscape.

Malls reported collection of less than 50% of rents in the second quarter - by far the lowest in the real estate sector - as retail landlords struggled to collect rent from these "non-essential" tenants. By comparison, housing, industrial, and technology REITs, along with self-storage and office REITs, all reported collection of more than 95% of rents. The majority of enclosed mall properties were closed during the peak of the coronavirus shutdowns in late March through mid-May, but essentially all mall REIT properties have now reopened. Collection rates have improved considerably in July, but commentary from these REITs suggests that a sizable percentage - perhaps half or more - of missed rents in the second quarter will ultimately remain uncollected.