Summary

- If I had to cherry-pick one period to be a Capital One bear over the past ten years, it would probably be the second quarter of 2020.

- From loan balances to interest margins and credit costs, I can't seem to find a good reason to be optimistic about this consumer bank.

- COF is too risky a value approach that I would rather stay away from ahead of earnings day.

- Looking for a helping hand in the market? Members of Storm-Resistant Growth get exclusive ideas and guidance to navigate any climate. Get started today »

- If I had to cherry-pick one period to be a Capital One (COF) bear over the past ten years, it would probably be the second quarter of 2020.

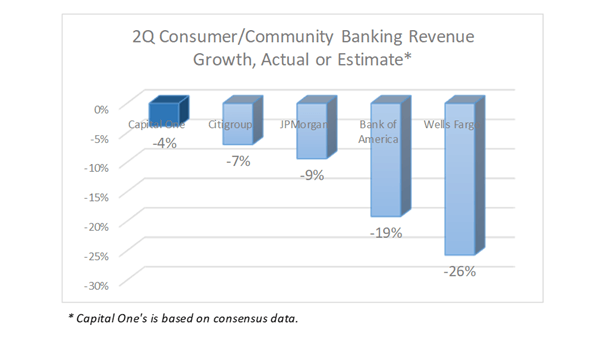

The consumer banking company is scheduled to report earnings on July 21, after the closing bell. Analysts don't seem too concerned about lack of top-line firepower, as consensus revenue decline currently sits at a mere 4%. EPS is projected to dig deep into negative territory, but the final number will depend greatly on the size of the credit reserve build-up that is expected to hit the P&L. Credit: Upgraded Points

Credit: Upgraded Points

Not much to justify optimism

From top to bottom, it is hard to find many reasons to be optimistic about Capital One's 2Q financial performance.

Big Bank earnings week already suggested that Consumer has been the softest segment among top diversified financial services companies, with Corporate Banking and Trading saving the space from an ugly wipeout during the period. As a reminder, Capital One is very much a "pure play" consumer bank that will not have the crutch of institutional clients to break its fall.

Starting from the top line, I expect to see a combination of bearish forces acting on the two main drivers of revenues: loan balances and interest margin. The former should be impacted by lower levels of consumer spending coupled with a defensive stance that has been leading to a decrease in household debt recently. On the margin side, a yield curve that is flatter and closer to zero will probably not help much. Just for reference, Bank of America's (BAC) net interest yield ex-global markets dropped by an eye-catching 71 bps sequentially in the second quarter.

Source: D.M. Martins Research, using data from multiple reports

When it comes to credit expenses, I would not dare guess what the added provision for losses might look like, but I expect it to be sizable. Not a single of the banks that I have followed during this earnings season seemed optimistic about the macroeconomic landscape going forward. I fear for Capital One the most, since it tends to have the lowest credit quality customer base - precisely the demographic group that I expect to bear the brunt of the COVID-19 crisis. See graph below on delinquencies and charge-offs between March and May.